- If the Fed Only Supports Strong Economic Indicators Amidst Polarization, the Next Recession Could Be Worse (1/2)

- US Economic Indicators Analysis: Real GDP maintains pre-corona growth, impact of government debt increase, mixed consumption indicators, strong employment but expected impact of illegal immigration decrease.

(Continued from Part 1 below)

The US government continues to steadily utilize debt and spend money, attempting to maintain the domestic economy in line with previous growth trends. They are only making a pretense of stopping illegal immigration, and this seems to continue having the effect of maintaining employment even with high interest rates. In a way, it feels like they are somewhat forcibly creating growth.

Some indicators still show strong performance, while others are already showing signs of slowing down. However, overall, the indicators that the Federal Reserve primarily uses as benchmarks, or those highlighted in headlines, such as GDP, Personal Consumption Expenditures (PCE), and total nonfarm employment, are largely showing strong performance.

As prolonged periods of increased money supply typically lead to increasing polarization (as seen throughout the history of capitalism), considering this, the normalization of overheating indicators might mean that some are already sensing signs of recession.

As shown in the article below from August, and in similar recent articles, about 60% of Americans report feeling a recession. Not 10-20%, but 60%, suggesting that a portion of the middle class and those below have already begun receiving signals of a weakening economy.

- 지표는 괜찮은데…미국인 60% "경기 침체"

- 공식적인 지표에선 미국 경제가 견조한 것으로 나타나고 있지만 실제 미국인들은 약 60%가 이미 경기침체라 생각하는 것으로 나타났다. ‘침체(recession)’와 체감 경기를 뜻하는 ‘분위기(vibe)’를 합쳐서 ‘

Currently, not only the US but also our domestic economy shows a similar situation. Negative signals are frequently observed, especially among small and medium-sized business owners.

Given that even the strongest US economy is showing such signals, it seems reasonable to assume that the actual economic situation in Europe, Korea, and other countries is even closer to a slowdown or recession.

- 빚 못갚는 소상공인 지속 증가…지역신보 대위변제 60%↑

- 고금리에 대출 상환 부담 가중 올해 소상공인이 갚지 못해 지역신용보증재단(지역신보)이 대신 변제한 은행 빚이 급증했다. 23일 국회 행정안전위원회 소속 더불어민주당 양부남 의원이 신용보증재단중앙회에서 제출받은 자료에

While benchmark indices primarily used by the Federal Reserve and the US government continue to show strong performance, voices from Federal Reserve officials are once again suggesting a slowdown in interest rate cuts. It seems the indicators suggest there’s no urgent need.

However, this ambiguous situation, where average or representative indicators appear good, but the lower and middle classes are already experiencing a recession, and is described as a prolonged "Goldilocks" economy, may have the adverse effect of completely depleting the stamina of the middle class and lower economic strata.

This could lead to a subsequent recession that is far deeper than normal, as a backlash. This was the content of the article below, that I wrote previously. That’s why I said that if this situation, disguised as a Goldilocks economy, continues, the subsequent recession will likely be extremely deep.

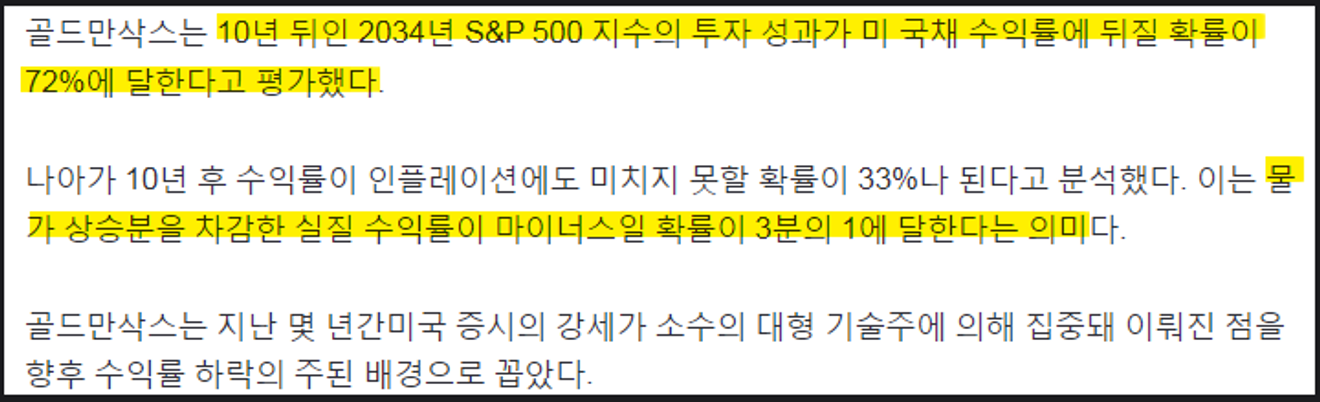

Goldman Sachs recently predicted that the US stock market is likely to underperform Treasury yields and inflation over the next 10 years. This means they believe that the stock market’s return, considering inflation, will be negative for the next 10 years.

However, if institutional investors actually consider this prediction to be highly probable, would the annual stock market return remain slightly positive, just below the bond yield? If some institutions think so, they would reduce their equity holdings and increase their bond holdings, which should normally lower the return on equity investments even more than predicted, wouldn't it?

Personally, I suspect that Goldman Sachs is laying the groundwork with a relatively mild prediction, keeping in mind the possibility of a second Great Depression-level crisis that I personally believe will occur within the next 10 years. Perhaps it's a way to leave a historical record that they made a rough prediction beforehand...?

- 골드만삭스 "향후 10년간 美주식 연평균수익률 3% 그칠 것"

- 장기 연평균 11%에 크게 못 미치는 수준…"소수 대형기술주가 강세 주도한 탓" 이지헌 특파원 = 미국 증시가 지난 10년간 누려왔던 장기 강세장이 끝났으며 향후 10년간 평균 수익률이 채권 수익률을 넘기 어려울 것

Comments0